Net sales are basically total sales less any returns or allowances. This is the net amount that the company expects to receive from its total sales. Some income statements report net sales as the only sales figure, while others actually report total sales and make deductions for returns and allowances. Either way, this number will be reported at the top of the income statement.

Managerial Accounting

With a high contribution margin ratio, a firm makes greater profits when sales increase and more losses when sales decrease compared to a firm with a low ratio. Investors and analysts may also attempt to calculate the contribution margin figure for a company’s blockbuster products. For instance, a beverage company may have 15 different products but the bulk of its profits may come from one specific beverage.

How to Calculate Contribution Margin?

For example, if the cost of raw materials for your business suddenly becomes pricey, then your input price will vary, and this modified input price will count as a variable cost. Typically, variable costs are only comprised of direct materials, any supplies that would not be consumed if the products were not manufactured, commissions, and piece rate wages. Piece rate wages are paid based on the number of units produced; for example, if the piece rate wage is $4 per unit and a worker produces 10 units, then the total piece rate wage is $40. Contribution per unit is the residual profit left on the sale of one unit, after all variable expenses have been subtracted from the related revenue.

Our Services

Thus, the total variable cost of producing 1 packet of whole wheat bread is as follows. Reduce variable costs by getting better deals on raw materials, packaging, and shipping, finding cheaper materials or alternatives, or reducing labor costs and time by improving efficiency. You pay fixed expenses regardless of how much you produce or sell. It includes the rent for your building, property taxes, the cost of buying machinery and other assets, and insurance costs.

This highlights the margin and helps illustrate where a company’s expenses. Variable expenses can be compared year over year to establish a trend and show how profits are affected. Direct materials are often typical variable costs, because you normally use more direct materials when you produce more items. In our example, if the students sold 100 shirts, assuming an individual variable cost per shirt of $10, the total variable costs would be $1,000 (100 × $10). If they sold 250 shirts, again assuming an individual variable cost per shirt of $10, then the total variable costs would $2,500 (250 × $10).

- Just as each product or service has its own contribution margin on a per unit basis, each has a unique contribution margin ratio.

- However, an ideal contribution margin analysis will cover both fixed and variable cost and help the business calculate the breakeven.

- Investors examine contribution margins to determine if a company is using its revenue effectively.

- Yes, the Contribution Margin Ratio is a useful measure of profitability as it indicates how much each sale contributes to covering fixed costs and producing profits.

- It represents how much money can be generated by each unit of a product after deducting the variable costs and, as a consequence, allows for an estimation of the profitability of a product.

What is the difference between the contribution margin ratio and contribution margin per unit?

Thus, \(20\%\) of each sales dollar represents the variable cost of the item and \(80\%\) of the sales dollar is margin. As you will learn in future chapters, in order for businesses to remain profitable, it is important for managers to understand how to measure and manage fixed and variable costs for decision-making. In this chapter, we begin examining the relationship among sales volume, fixed costs, variable costs, and profit in decision-making. We will discuss how to use the concepts of fixed and variable costs and their relationship to profit to determine the sales needed to break even or to reach a desired profit. You will also learn how to plan for changes in selling price or costs, whether a single product, multiple products, or services are involved. Contribution margin income statement, the output of the variable costing is useful in making cost-volume-profit decisions.

Let’s take another contribution margin example and say that a firm’s fixed expenses are $100,000. Other financial metrics related to the Contribution Margin Ratio include the gross margin ratio, operating margin managing dishonoured payments in xero ratio, and net profit margin ratio. These ratios provide insight into the overall profitability of a business from different perspectives. A firm’s ability to make profits is also revealed by the P/V ratio.

For instance, increasing production can spread fixed costs over more units, potentially lowering the cost per unit and boosting profit margins. However, this strategy only works within what financial analysts call the “relevant range” of production levels where these cost relationships hold true. As mentioned above, the contribution margin is nothing but the sales revenue minus total variable costs. Thus, the following structure of the contribution margin income statement will help you to understand the contribution margin formula. This demonstrates that, for every Cardinal model they sell, they will have $60 to contribute toward covering fixed costs and, if there is any left, toward profit. Every product that a company manufactures or every service a company provides will have a unique contribution margin per unit.

Thus, the contribution margin ratio expresses the relationship between the change in your sales volume and profit. So, it is an important financial ratio to examine the effectiveness of your business operations. Now, this situation can change when your level of production increases. As mentioned above, the per unit variable cost decreases with the increase in the level of production. Sales revenue refers to the total income your business generates as a result of selling goods or services. Furthermore, sales revenue can be categorized into gross and net sales revenue.

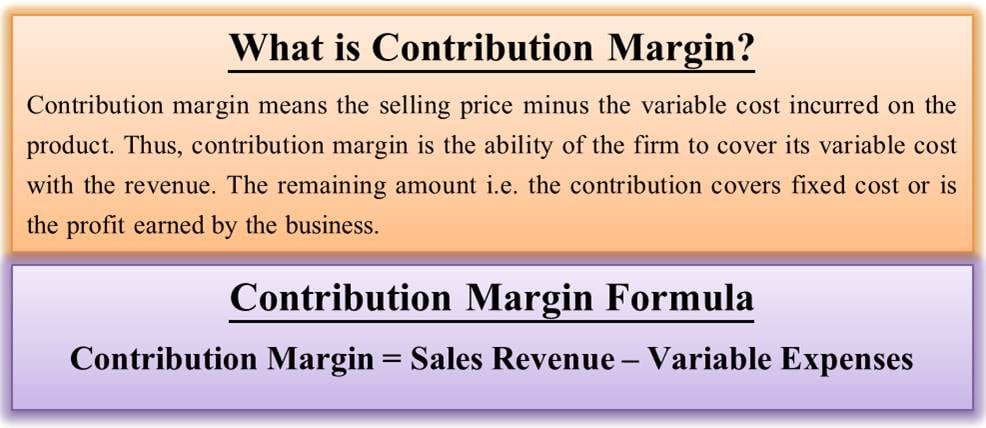

Contribution margin analysis is the gain or profit that the company generates from the sale of one unit of goods or services after deducting the variable cost of production from it. The calculation assesses how the growth in sales and profits are linked to each other in a business. The first step to calculate the contribution margin is to determine the net sales of your business.

Management must be careful and analyze why CM is low before making any decisions about closing an unprofitable department or discontinuing a product, as things could change in the near future. A contribution margin analysis can be done for an entire company, single departments, a product line, or even a single unit by following a simple formula. The contribution margin can be presented in dollars or as a percentage. You need to work out the contribution margin per unit, the increase in profit if there is a one unit increase in sales. In effect, the process can be more difficult in comparison to a quick calculation of gross profit and the gross margin using the income statement, yet is worthwhile in terms of deriving product-level insights. Using the provided data above, we can calculate the price per unit by dividing the total product revenue by the number of products sold.